Cancellation of GST Registration means the GST Number or GSTIN of a registered taxpayer becomes inactive. The taxpayer will not have to pay or collect GST or file returns, after the cancellation of Registration.

Index

- Who can apply for the Cancellation of GST Registration?

- Process for Cancellation of GST Registration on GST Portal

Who can apply for Cancellation of GST Registration?

Tax Officer– Suo Moto Cancellation

A tax officer may initiate cancellation of registration in the following cases.

- Taxpayer is not doing business from his registered place of business.

- The taxpayer issues tax invoices without selling goods or services.

- The taxpayer violates the provisions of the act or rules issued by the GST Council.

- GST Registration was obtained either by fraud or misstatement of facts.

- A taxpayer under the regular scheme has not filed returns for a continuous period of 6 months.

- Taxpayer under Composition Scheme has not filed returns for three consecutive tax periods.

Taxpayer – Voluntary Cancellation

A registered taxpayer may initiate the cancellation of registration on the GST Portal in the following cases.

- The taxpayer has either closed or discontinued his business.

- The taxpayer has transferred his business due to amalgamation, merger, de-merger, sale, lease, etc.

- There is a change in the constitution of business leading to change in PAN. For example, proprietorship converted to a private limited company.

- The taxpayer has taken Voluntary Registration but did not commence any business within a specified time.

- If a taxable person is no longer liable for registration under the GST Act.

- The taxpayer is no longer liable to pay tax.

- Application for cancellation, in case of voluntary registration, can be done only on after expiry of one year from the registration date.

Legal Heirs

The legal heirs can file for cancellation of registration of the proprietorship firm in case of death of a sole proprietor. The taxpayer or legal heir can cancel GST Registration by filing Form REG-16 on the GST Portal.

Process for Cancellation of GST Registration on GST Portal

- Login to GST Portal

Go to the GST Portal and login using a valid username and password.

- Go to Services > Registration > Application for Cancellation of Registration

Navigate to the option ‘Application for Cancellation of Registration’ under the tab Services.

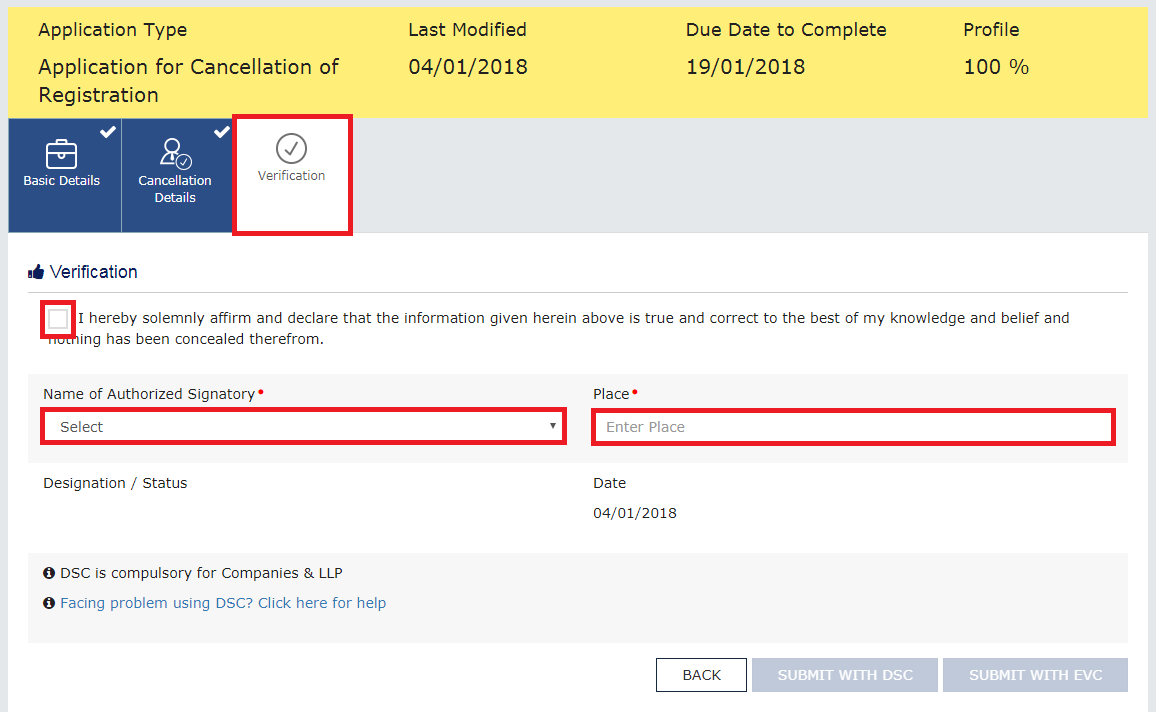

- Basic Details, Cancellation Details, Verification

The cancellation form comprises of 3 tabs – Basic Details, Cancellation Details and Verification.

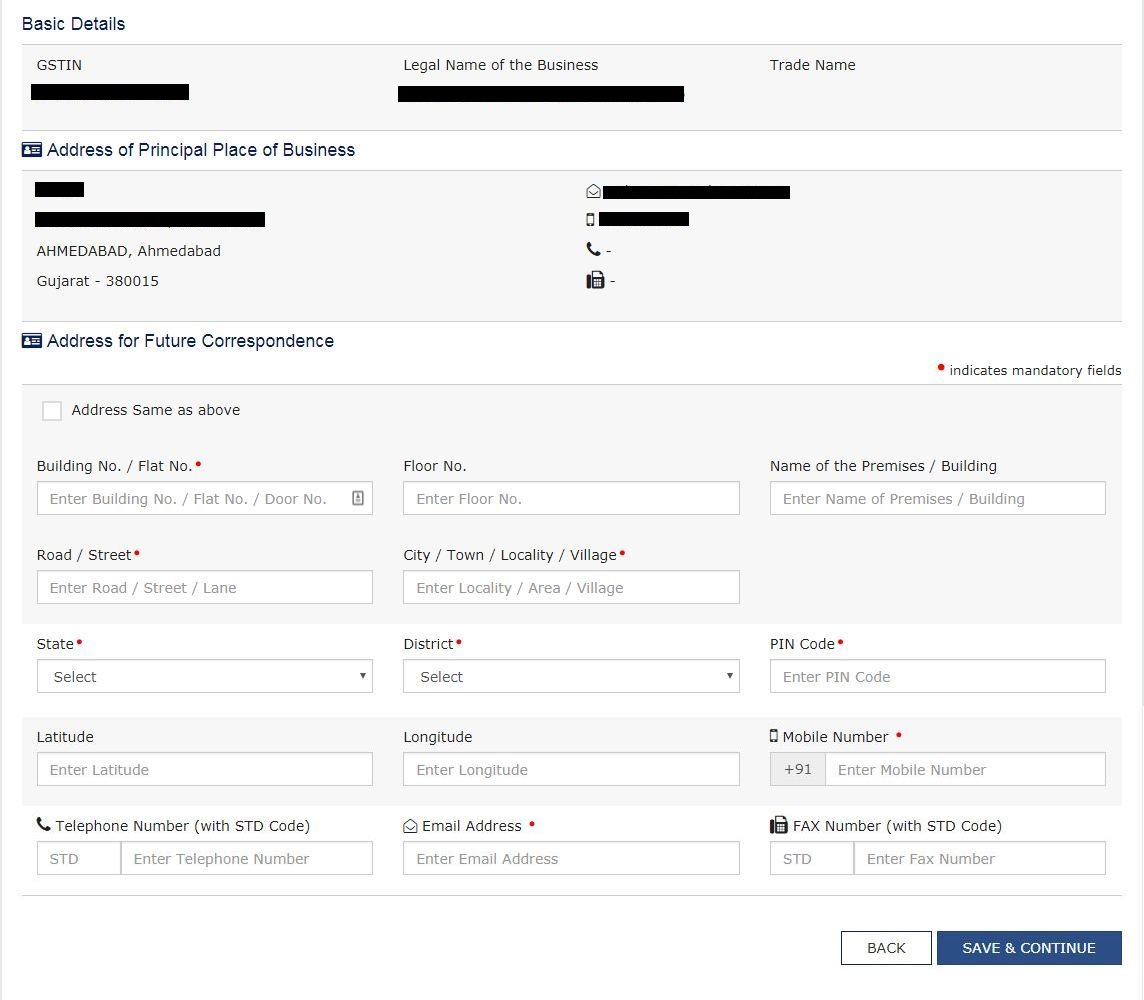

- Enter details in tab – Basic Details

Under the first tab of Basic Details, enter the following:

a. Address of future correspondence,

b. Mobile Number,

c. Email Address.

- Enter details in tab – Cancellation Details

Under the second tab of Cancellation Details, select the reason for cancellation from the drop-down. For each reason selected, enter additional details as mentioned in the table under next topic.

- Verification

Under the last tab of Verification, select the name of authorised signatory from the drop-down and enter the place of declaration. Submit the application using DSC or EVC.

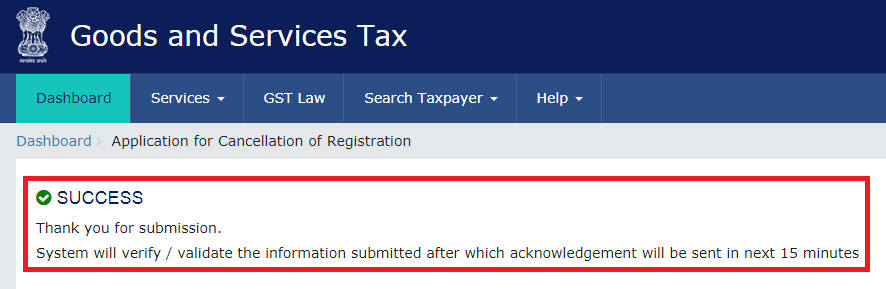

- Success Message

A success message is displayed on the successful submission of the application.

- Track status of application

To track the status of the ARN, go to Services > Registration > Track Application Status.

Cancellation of GST Registration – Reason & Additional details

|

Reason for cancellation |

Additional details required |

|

Change in constitution of business leading to change in PAN |

|

|

Transfer of business on account of amalgamation, merger, demerger, sale, leased or otherwise |

|

|

Ceased to be liable to pay tax |

|

|

Discontinuance of business / Closure of business |

|

|

Others |

FAQs

1. The taxpayer will not have to pay GST anymore

2. For certain businesses, registration is mandatory. If the registration is canceled and business still continues, it will be considered as an offense and heavy penalties will apply.

In the case of a voluntary registration, the taxpayer can apply for cancellation only after the expiry of one year from the date of registration.

In order to change the details of your registration, you need to visit the GST official portal. Go to Services > Registration > Amendment of Registration Non-Core Fields. Select the desired tab and make the necessary changes.

Hey @HarshitShah

GST Registration is the application for GST Number or GSTIN(GST Identification Number). Under the GST(Goods and Service Tax) Regime, it is mandatory for to have GSTIN to collect, pay GST and claim the Input Tax credit.

For GST registration, the dealer has the following options:

Voluntary Registration: The business does not have the liability to register under GST, however, can apply for GST Registration. This usually is when the businesses are willing to take advantage of the Input Tax Credit facility

Registration under Composition Scheme: Composition scheme is a voluntary and optional scheme for registering under GST. Under the composition scheme, the compliance is simpler and lesser returns are to be filed. The tax is to be filed at a fixed rate. If the business turnover is in between INR 40 Lakhs and 1.5 Crores, they can opt for GST Registration under Composition Scheme

No Registration: In the case, when your business does not fall under the conditions for compulsory registration you do not require GST Registration

Hope this helps!

What documents do I need for a new GST number?

Hey @SonalYadav

To get a GST Number or GSTIN in India, you will be required to Register under GST(Goods and Service Tax)

Usually, you receive the GST Number within 4–7 days of GST Registration application is submitted.

Follow these steps to register under GST on GST Portal:[1]

PART A of the GST Registration Application

Now let’s start with the PART B of the GST Application

The PART B of GST Application has various tabs. You will be required to enter the relevant details and upload relevant documents.

Usually, GST Number or GSTIN is allocated within 4–7 days from submitting the GST registration application.

Hope this helps!

Footnotes

[1] GST Registration Process online on GST Portal: Guide | Help Center | Quicko

Hey @Shweta_Saini

You can opt out of Composition Scheme from your account on GST Portal. Once the taxpayer type is updated to Regular in your profile, you can start filing GST Returns under the regular scheme. If you are facing any issues while making the withdrawal application, you can create a grievance on the GST Portal.

Do let us know if you have any further queries.

I want to be able to claim input tax credit for GST paid. Should I opt for the GST composition scheme or regular scheme?

Hey @Joe_Fernandes

If you wish you claim Input tax credit, you should opt for GST Regular Scheme.

Read more about the difference here.

1.composite scheme dealer inward supplies detailes(purchases invoices ) uploaded manadatory show in gstr4 annual return.

2.composite dealer late fees and interest calculate procedure.

Hi @Sundaraiah_Kollipara,

As per Rule 62(3)(a) of CSGT Rules, 2017 (Part A_Rules) A composition taxpayer has to furnish

As per the instructions given below FORM GSTR-4 of CGST Rules, 2017 (Part B_Forms), the following information relating to inward supplies (rate-wise) needs to be provided

But as per clarification by GST department, when the auto-population feature for inward supplies which was available on the GST portal was not working. Reporting in table 4A of GSTR-4 is not mandatory.

Further, late fee of Rs. 200 per day is levied if the GSTR-4 is not filed within the due date. The maximum late fee that can be charged cannot exceed Rs. 5,000. Interest is also calculated at rate of 18% p.a on tax liability.

You can read our below articles for more insights:

A retail pharmacy store dealer composite scheme registered in gst act recently.dealer purchase of medicines different tax rates(1 ,12,18 percent)and sale to counter sales through on Google pay and phone pay online mode and cash mode sales two types amounts received.my doubt: dealer how to accounting entry passed procedure in books

@AkashJhaveri @Kaushal_Soni @Divya_Singhvi @Laxmi_Navlani can you?